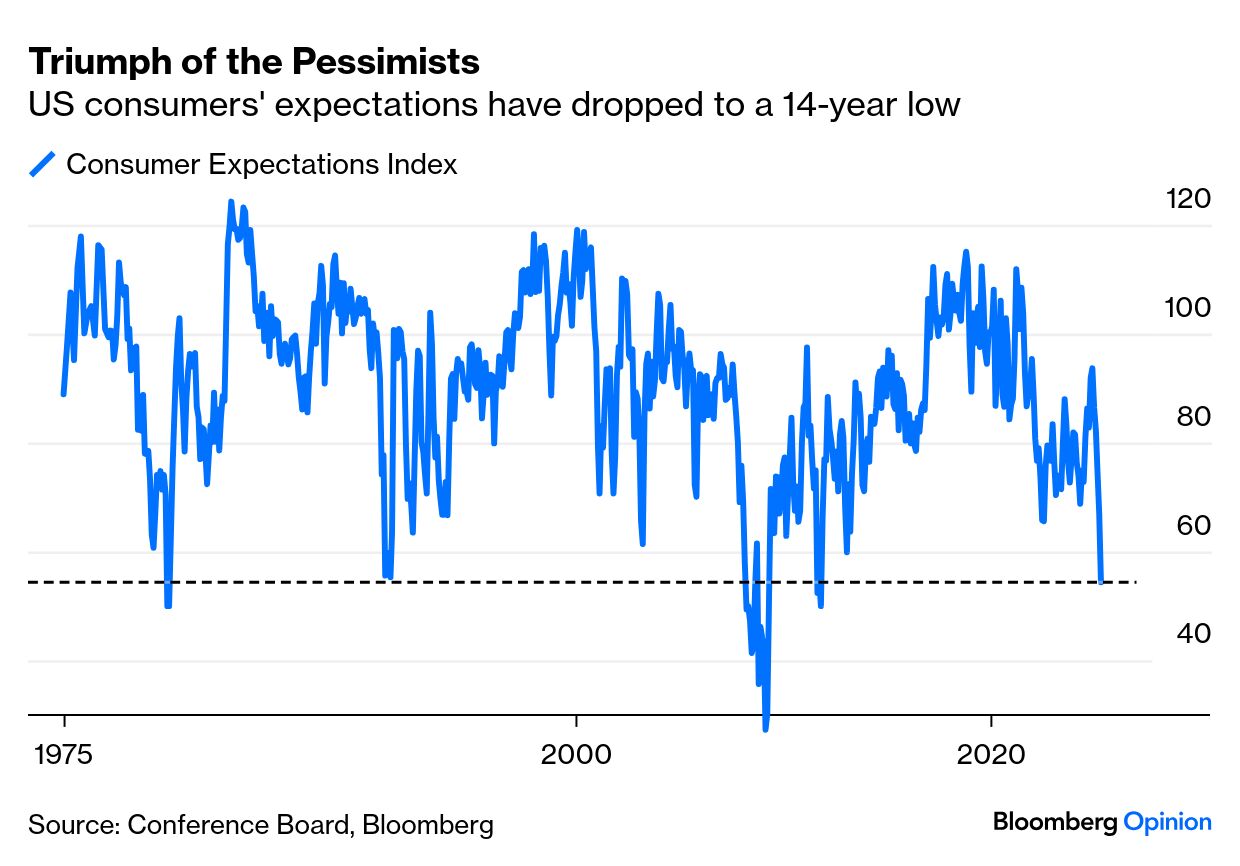

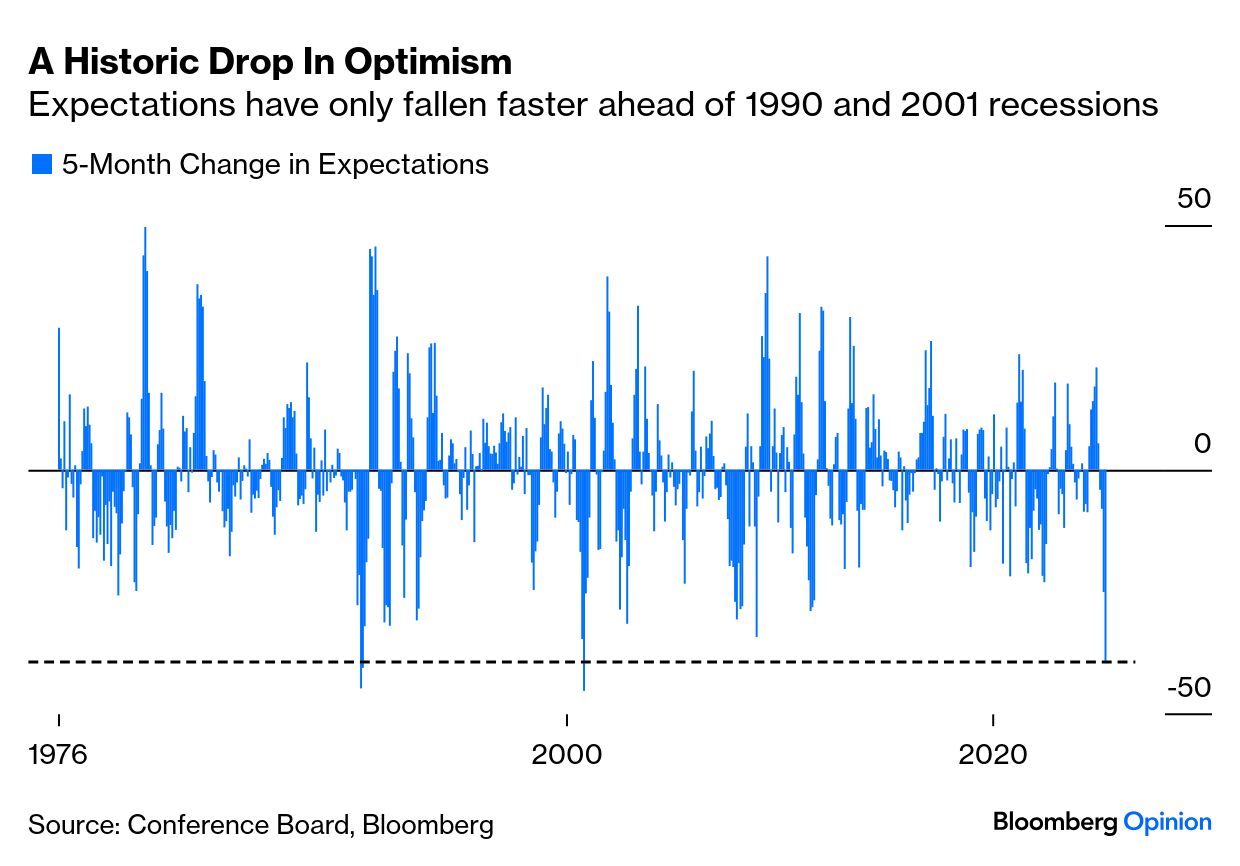

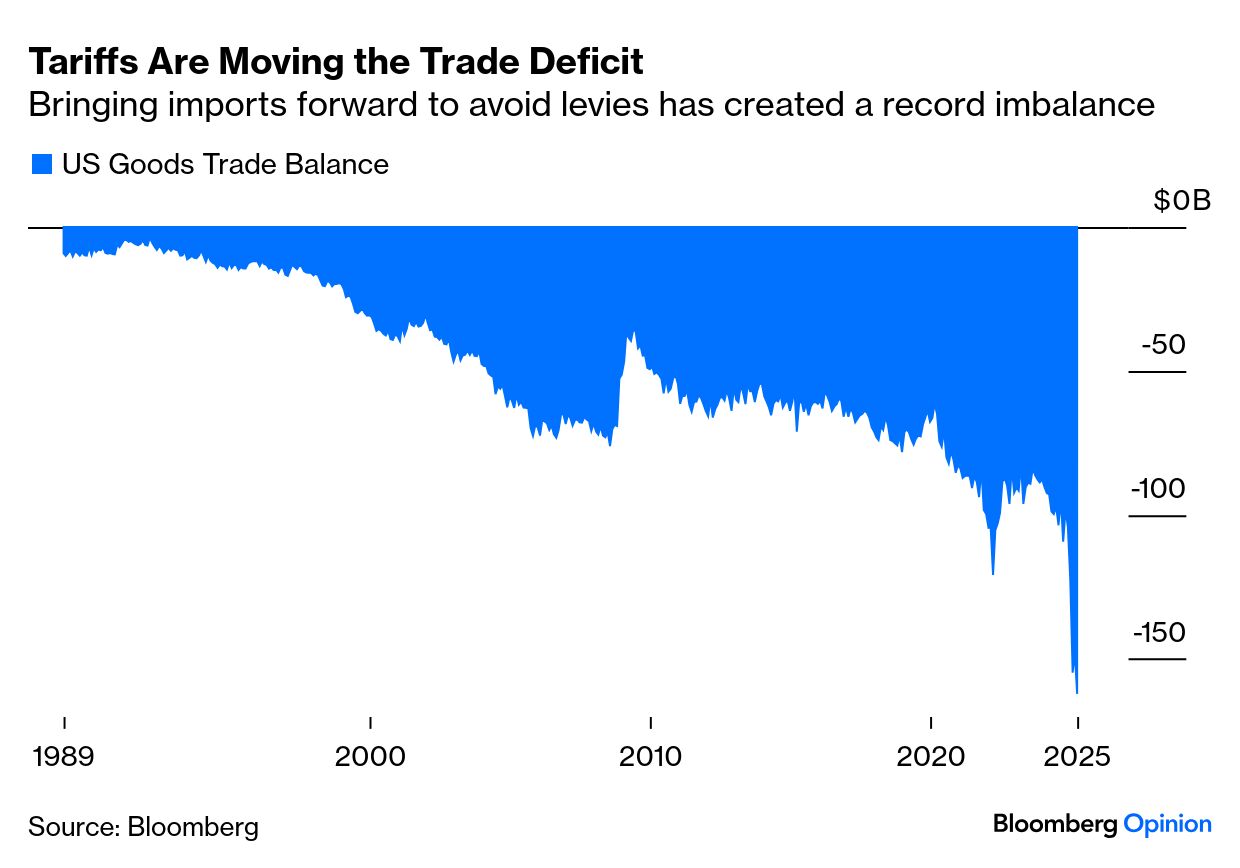

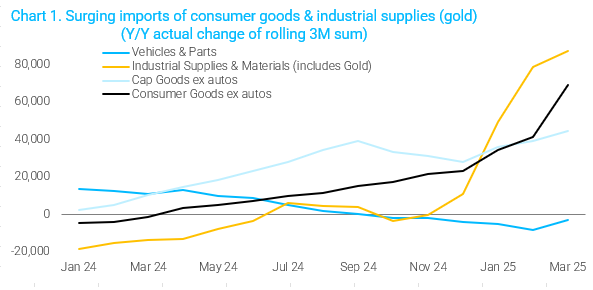

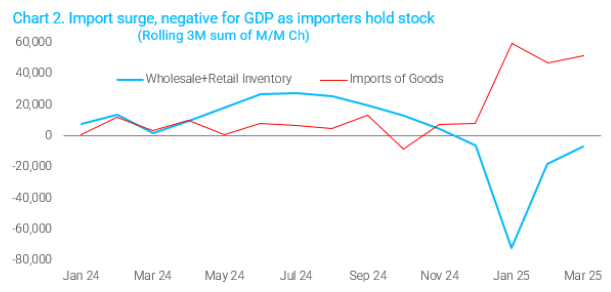

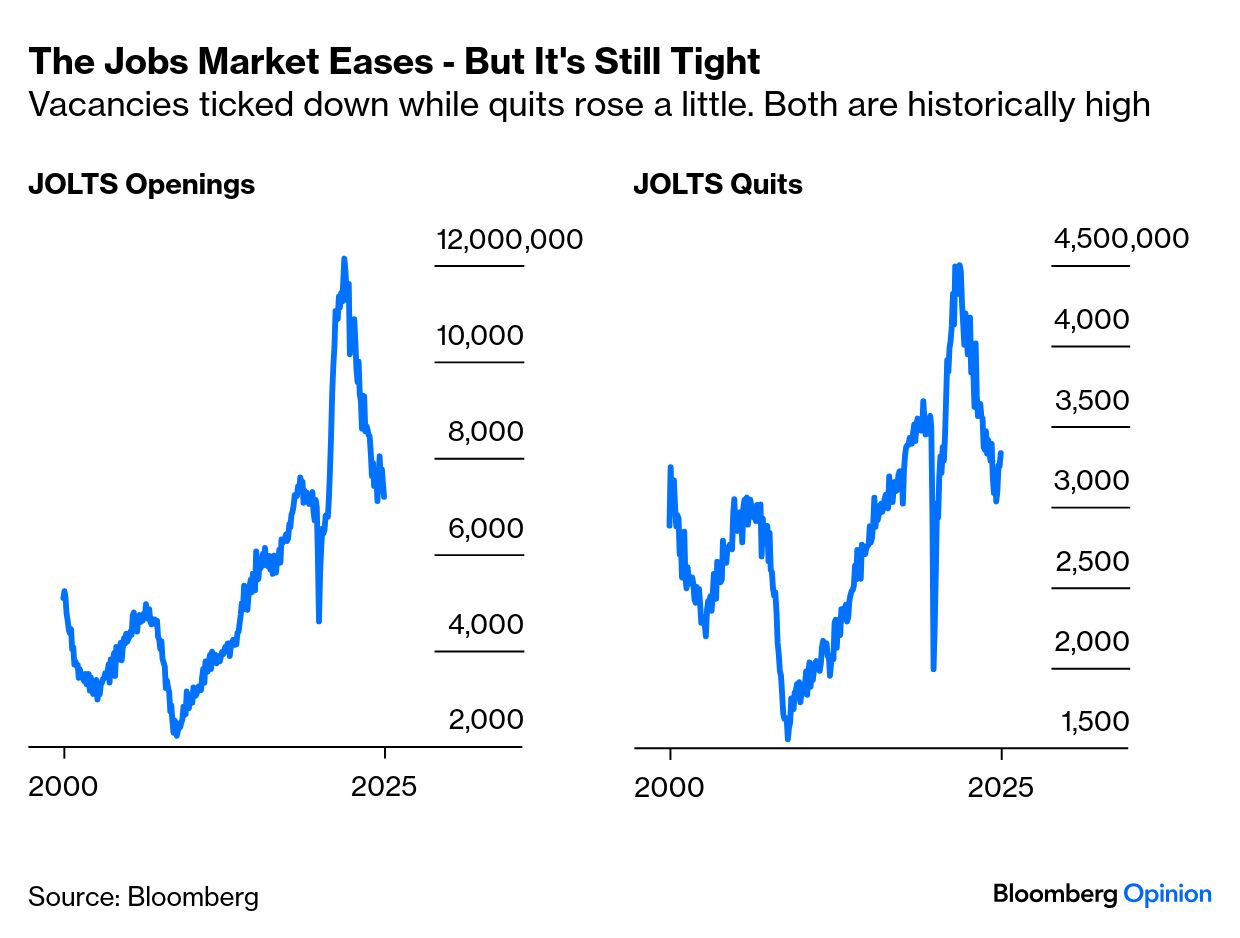

| The economic data are flowing again, but colored by the suspended animation as we wait for tariffs to bite. Some numbers lag, so tell us nothing about behavior since the April 2 Liberation Day announcement; some are soft, based on opinions; and the data that could really make a difference will be hard. As it stands, the soft data tell us that the US is braced for catastrophe, the lagged data suggest the economy was in decent shape coming into the tariffs, and the hard data show that companies are doing a lot to front-run the levies when they arrive. Firm conclusions are difficult. The market, however, is betting on a recession. These are the odds on Polymarket: Why so convinced? Starting with the soft data, the latest Conference Board measure of US consumer confidence was atrocious, particularly the forward-looking elements. This is what has happened to consumer expectations over the last 50 years: It’s very rare for consumers to be this pessimistic. They’ve only been this negative during the stagflation in 1980, and the Global Financial Crisis era. It’s hard to explain their sentiment away. Political polarization may be a factor, but nobody thinks Democrats are getting their message out better than the Republicans. The speed of the descent is also historic, with the index shedding 38 points in the five months since November, when Trump’s win created optimism. Only twice before have expectations fallen so far in a five-month period: in early 2001, and in the autumn of 1990. Recessions followed both times: Lows on this measure tend to be good times to buy stocks, and sentiment cannot keep falling this fast. Contrarians can find reassurance in this survey. As for hard data, the latest balance of trade for goods is extraordinary. The prospect of tariffs prompted a massive splurge as importers hurried to get in their orders before levies take effect. The result is by far the deepest deficit on record. These are hard numbers, but very unlikely to be sustained: This is overwhelmingly driven by attempts to bring in consumer goods from China. Flows of gold bullion, which also count as imports, have also distorted the figures a little. This chart from Steven Blitz of TS Lombard shows the breakdown: There’s a widespread assumption that rising imports subtract from gross domestic product, thanks to the classic Economics 101 GDP formula, [1] which is C + I + G + (X - M), where X stands for exports and M for imports. It’s not that simple, as an exasperated post from former colleague Noah Smith should explain. Imported goods generally show up as consumption or investment, so it’s necessary to subtract them to avoid double counting. That means that when Commerce Secretary Howard Lutnick suggested in a CNBC interview that cutting the trade deficit by 25% would mean an extra percentage point of GDP growth, he may well be wrong — unless the imports are replaced one-for-one by goods made in the US. However, in this case, it’s fairly clear that imports are displacing some domestic production, as companies divert cash to beat tariffs. As Blitz shows in this chart, importers are holding on to their inventory: Lagging data on the job market came in the Job Openings and Labor Turnover Survey (JOLTS) for March. Vacancies dropped a bit, quits rose a bit and there was no bump in layoffs. The labor market isn’t extremely tight like it was during the inflation of 2022. It’s not very loose either, and certainly doesn’t compel the Fed to cut rates: This is the assessment by Carl Weinberg, chief economist at High Frequency Economics: In short, there is not very much wrong here. BLS repeatedly uses the words “little changed” or “unchanged” to describe the elements of this report. We see no reason to dispute its assessment. No sign of recession can be found. Companies seem to be holding on to workers until they see how tariffs shape up. We are still waiting for a surge in layoffs.

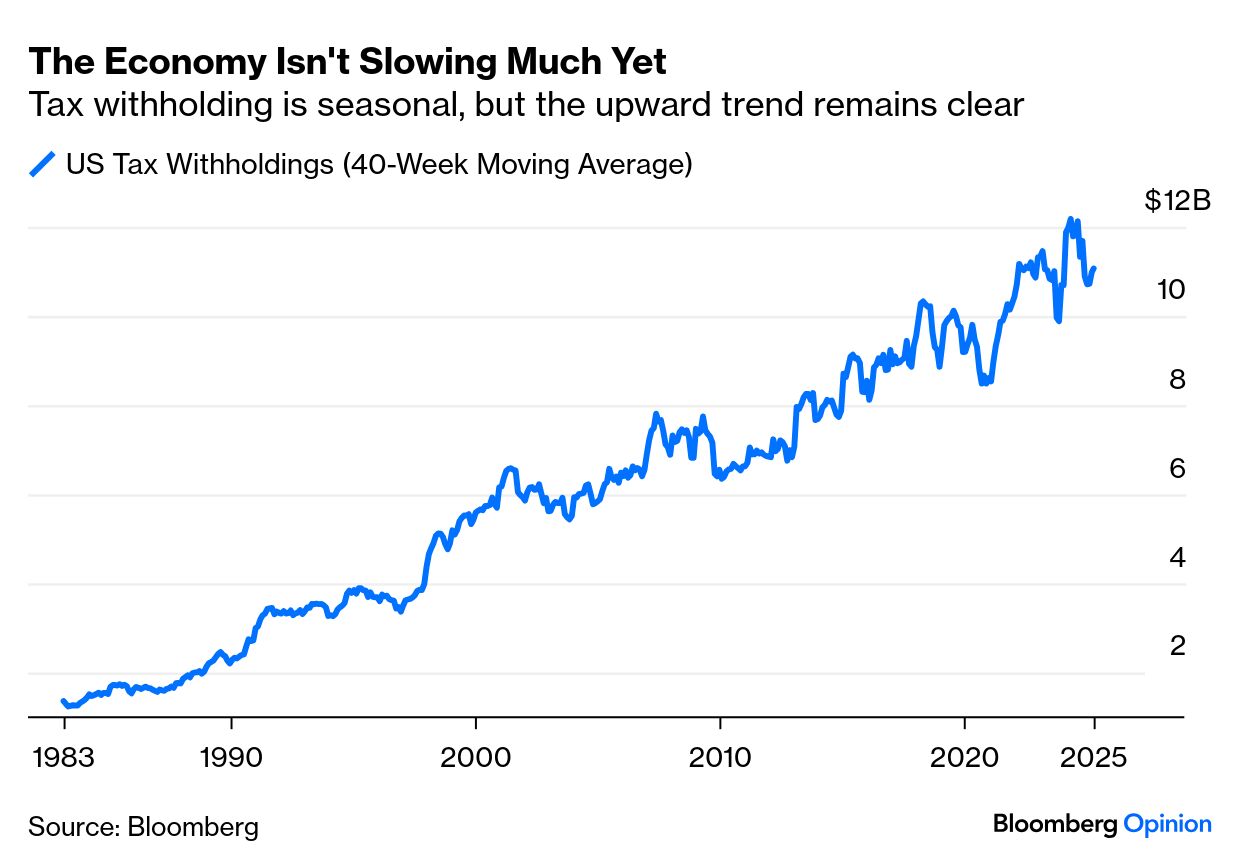

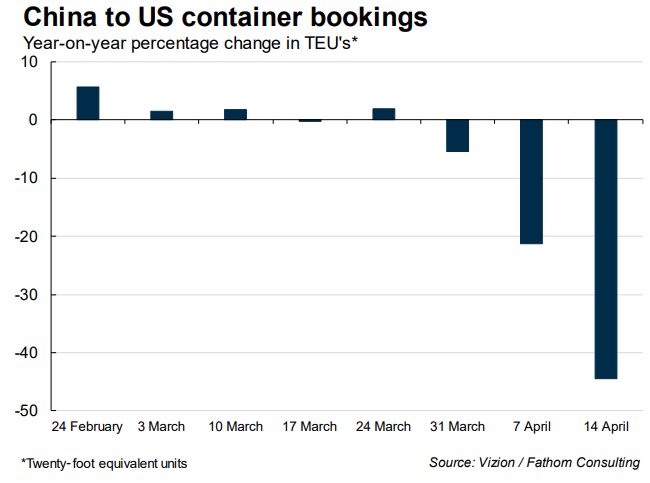

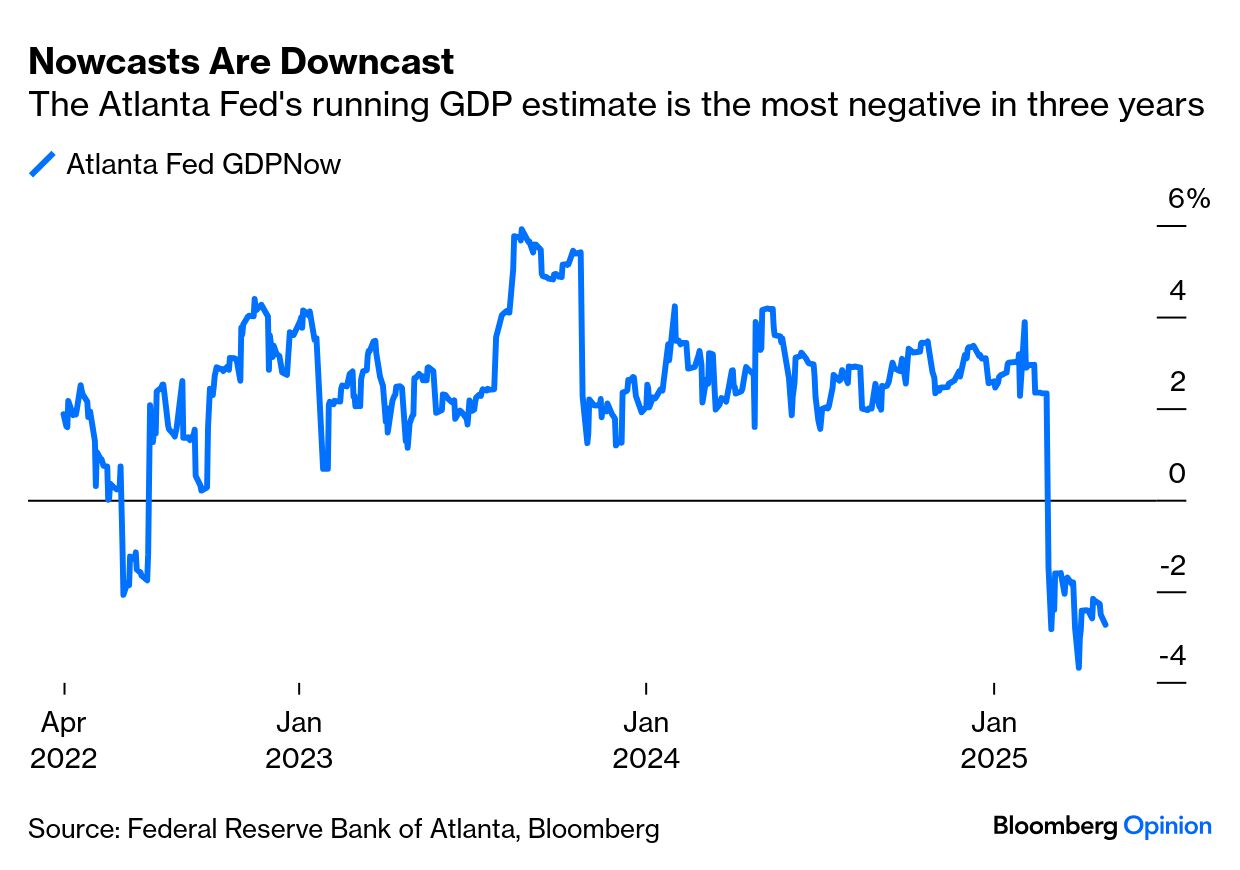

Less lagged data will come Friday, with non-farm payrolls for April. For now, we know that the labor market wasn’t in particularly bad shape on the eve of Liberation Day. Real-time data are very noisy but also suggest that the economy hasn’t stopped humming along yet. Larry Adam, chief investment officer of Raymond James, points to tax withholding numbers, which show that tax receipts are continuing on an upward trend. That wouldn’t be happening if the economy was already contracting: Put all of this together, however, and the chance of a recession looks much higher, with everyone now waiting to find out the impact tariffs have on deliveries, particularly from China. The recent import splurge means it will be a while before we have empty shelves, which could be deadly for the economy. But another almost real-time indicator, of container ship departures from China, suggests that it will come to that eventually unless there’s a climbdown. Vizion keeps a handy tariff-tracking blog to monitor weekly traffic. This chart is from Elisabeth Werenskiold of Fathom Consulting, and demonstrates a total collapse in shipments earlier this month, once the 145% tariff rate had been announced: Companies have taken enough evasive action to suggest that it will be some time before all of this shows up in truly current hard data. But the Atlanta Fed’s widely followed GDPNow nowcast seems confident that the point of no return has been passed: If in a few months the hard data don’t confirm a slowdown after such a nosedive in sentiment, markets should rebound in a big way. But certainty is a way off. To celebrate 100 days of Trump 2.0, Bloomberg Opinion is breaking out in all media. We’ll be holding a live Q&A on the market with me, Jonathan Levin and Allison Schrager. (I’m also grateful to Allison for explaining why Amazon absolutely should list the cost of tariffs, meaning that I didn’t have to. Of course they should.) Please join us: And you can also catch up with my video on the way the dollar has weakened under Trump 2.0 so far, and how it mirrors Ronald Reagan’s first 100 days: And should you wish to follow me on Twitter, my account has been restored after a few weeks under the control of a troll. I’m @johnauthers. Don’t even think of not using two-factor authentification… |