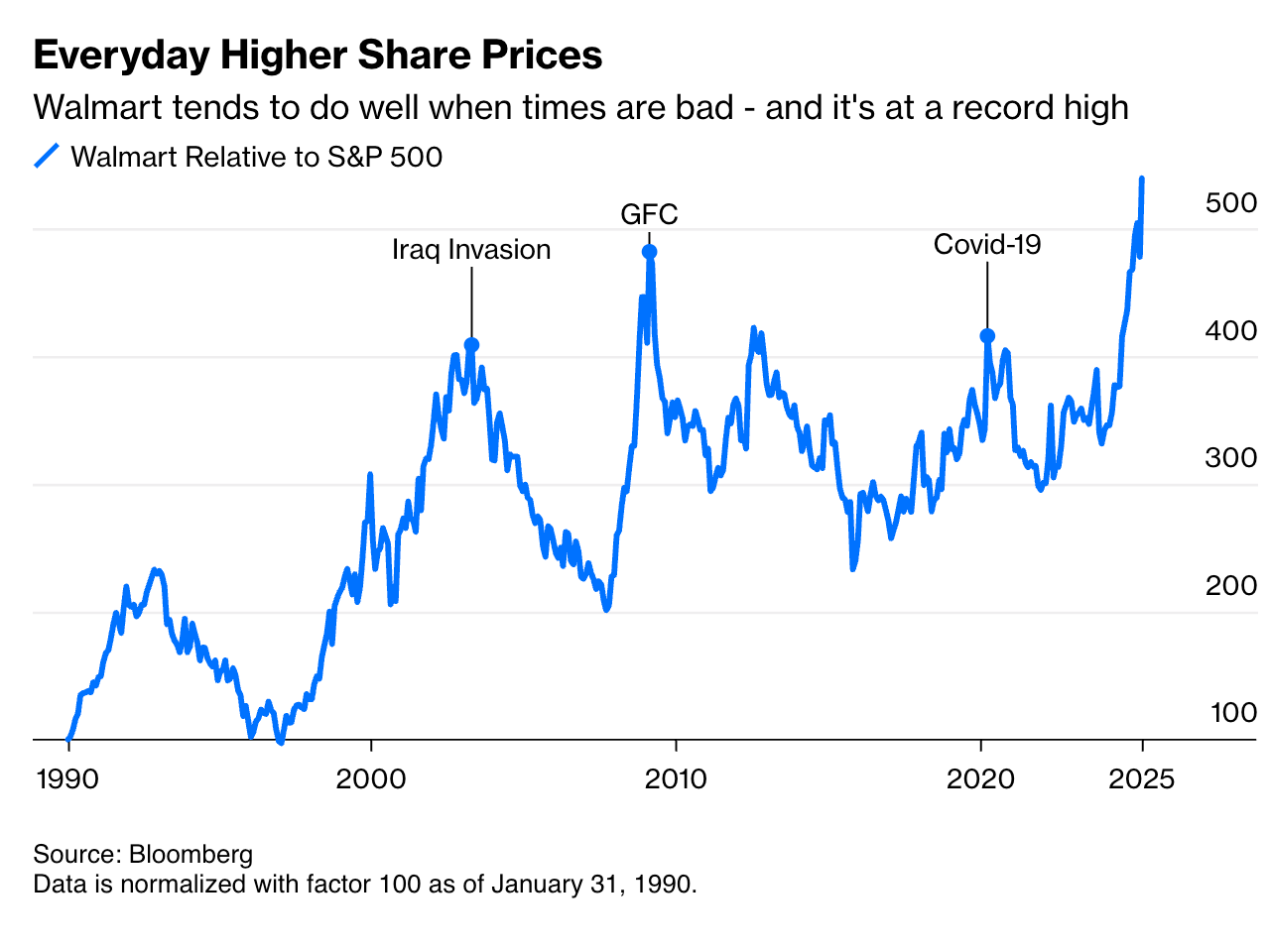

| The best case scenario that I outlined in March, one in which both inflation and slow growth are short-lived, is pretty much out the window now. Where there was an average US tariff rate of maybe 2.5% previously, the effective rate is now more than 10 times as large, at 28%, according to Yale’s Budget Lab. It hasn’t been that high since 1901. The new best case we’re all hoping for is a situation where slower growth doesn’t tip into recession. That could happen because of some combination of consumer resilience, pro-growth policies elsewhere in the Trump agenda and a rollback of the most outlandish tariff rates. Maybe then we get just a short period of below-trend growth, earnings forecast cuts and a step-up in the price level of tariffed goods. I think the (near-) correction we’ve seen in stocks adequately prices in this outcome. That would imply that once we’re back to better growth, the dip buyers will come back and stocks can continue to rise. But I think that is unlikely to happen. And where I gave it maybe a 40% chance in March, I’d decrease that to 25%. The reason is that Trump’s belief in the power of tariffs is firm and nobody in the administration appears to be trying to dissuade him. The market still wants to believe that some combination of lower stock prices and sinking poll numbers will pull him away from them, as the auto tariff tweaks suggest. But he talked so much about tariffs during the campaign and has risked so much already that he cannot fully capitulate and save face. He once went so far as to promote a video arguing that he was intentionally tanking the stock market, and when it slipped on Wednesday after the bad GDP data came out, he blamed former President Joe Biden and said his tariffs will release a US production boom as companies shift to the US to avoid them. Still, given the pause and floated carve outs, it’s still up in the air where tariff rates will settle. Given bipartisan distrust of China, those are likely to be stickiest. We have already heard many stories of cargo shipments falling off dramatically to West Coast US ports like Long Beach, Los Angeles and Seattle. So this disruption is likely to last months, and that means shortages and higher prices for months, too. The first question is whether the regressive nature of China-focused tariffs helps prevent a recession, given the economy’s increased dependence on the upper 10% of households for growth. We will find out when the shortages appear, likely beginning in mid- to late-May. The second question is whether there are knock-on effects from a recession that increase its severity. These would include de-dollarization, fire sales of illiquid private market assets, and negative wealth effects from a plunging stock market. The US hasn’t had a real recession since 2009, given that the pandemic downturn triggered an unprecedented government response that quickly offset the toll. So it’s difficult to say how fragile the system is if we face a contraction without that sort of extraordinary stimulus. One last look at Walmart as a guide | Walmart is worth focusing on as an example. It has a rich valuation for perhaps two reasons. The first is that all stocks have seen their valuation multiples rise prodigiously during the bull market that started in 2009. The second is that Walmart benefits when economic uncertainty increases as portfolios become more defensive. Look at this chart from my colleague John Authers, for example. John notes that: Walmart Inc. was the only stock in the S&P 500 that rose between the market peak in 2007 and the low in 2009. When it is beating the overall market, it’s a clear sign that investors don’t think much of the economy. And Walmart is doing well of late, hitting an all-time relative to the market.

That’s not a death sentence for market returns, of course, since Walmart’s relative valuation peaked during the QE episodes in the early 2010s before the rest of the market caught up as the US economy enjoyed a long boom. But it tells you something about market psychology. To me, it suggests that while investors acknowledge challenges ahead, they want to remain fully invested in stocks. For example, during the selloff on early Wednesday, as every stock market sector ETF from iShares was down, consumer staples were marginally higher. They are simply rotating to a more defensive allocation until the risks pass. Walmart has benefitted. Yet given the panic selling we’ve witnessed on multiple occasions over the past year on the mere hint of a recession, investors are clearly fearful. These false alarms end with many buying the dip. An actual recession will be met with a torrent of selling as investors move to mimic Warren Buffett, who already has his largest cash allocation ever. In the meantime, we just have to wait and see how this all plays out. It’s the showdown with China that will probably decide investors’ fate. And what’s now become a war of attrition more than a game of chicken favors those with a long-term perspective. That seems to tilt the odds in favor China — and against a comeback for US equities. |