| With 100 days complete, and Liberation Day a month in the past, a new date now looms on the horizon: July 8, when the 90-day pause on the tariffs known as “reciprocal” is due to expire. Without agreements or a unilateral climbdown from the Trump administration, tariffs will on that day return in full force across the world. The recovery of risk assets implies great confidence, then, that deals can be reached. Is it justified? Key to the confidence is that the president has already blinked several times. The proliferation of stories about talks toward deals — even if none of them has any specific details — further shows that the administration wants to negotiate. For example, the European Union will come forward with a proposal next week; China says that the US has approached it (while denying Trump’s assertion that Xi Jinping has already been in touch); and India has high hopes of a good settlement. But there are also plenty of hints that deals aren’t going to be easy. British objections to US chlorinated chicken continue to stand in the way of a US-UK deal; the EU is also discussing retaliation plans, while its negotiators are less confident than their US counterparts. And the basic problem remains: trade talks take time and barely two months remain, in which the US must thrash out deals with virtually every other country on the planet. Any further extension will leave the market, and other trade negotiators, convinced that Trump has folded. So deals must be done by then. Viktor Shvets of Macquarie Capital suggests that the market has set itself up for disappointment: Trade agreements are not trade deals. Long-term sustainable agreements require years of negotiations, with teams from both sides reviewing the entire relationship, from raw materials and intermediate to final goods, with some compromises (usually agriculture and national security) baked into the final agreement. In addition, there has to be a belief that both sides will broadly comply. What is happening today more closely resembles negotiations of temporary ceasefires than lasting peace.

Another issue: the US’s problems with many of its bigger trading partners are largely illusory, as decades of post-war negotiations have left most countries with low tariff barriers no higher than those levied on them by the US. It's not obvious what they have to offer unless the US strays into what Jean Ergas of Tigress Financial Partners describes as “reparations” — looking for payment for past help. As the Canadian election demonstrates, it will be very hard for democratically elected politicians to go along with anything that looks like extortion or a shakedown. However, they might be prepared to go through with some play-acting to help the US walk back. “In theory,” says Signum Global Advisors’ Andrew Bishop, “markets could find just as much solace in fake trade deals as in real ones.” Such announcements would signal that both Trump and his counterparts shared a desire to “pretend” and therefore also demonstrate that there was no need to fear tariffs in the future. A precedent has already been set with February’s negotiations with Canada and Mexico after the US proposal to levy tariffs on them to prevent fentanyl coming over the US border. Those tariffs went away, and the stock market rallied, after transparently meaningless undertakings. For example, it was announced that Canada would station 10,000 personnel to the border — and Canadian sources then made clear that those 10,000 had already long been in place. Will world leaders really be cynical enough to go through with multiple exercises like this? The US is now looking to draw up memoranda of understanding (MOUs), which would “offer a broad architecture for further deals.” Put differently, they wouldn’t be deals in any meaningful sense, but they would give the US the necessary fig leaf to leave tariffs at only the baseline 10%, rather than imposing the “reciprocal” tariffs on top. Beacon Research draws an analogy between the US and Oprah Winfrey: “You Get an MOU! And You Get an MOU!” Armed with an MOU, the US counterparts would have far less incentive to thrash out deals that would take years to organize in any case. So the base case on which the market is operating is that the US and other countries will go along with a charade to help the president out of difficulty. There are two problems with this. The first is that China is by far the most important and difficult case, there is no way Xi will go along with a game show ritual like this. And it appears at present that the impasse can only be broken by a unilateral move from the US to bring down tariffs from the current untenable 145%. Time is of the essence. For everyone else, the uncertainty would remain. To quote Macquarie’s Shvets again: Despite some deals and concessions, business confidence is unlikely to be restored. Outside punitive tariffs (e.g. China-US), it is not about the level but consistency. Rapid-fire announcements that are delayed, only to be reinstated in a different form, are likely to keep businesses on the edge, delaying investments or running these at a lower than otherwise rate.

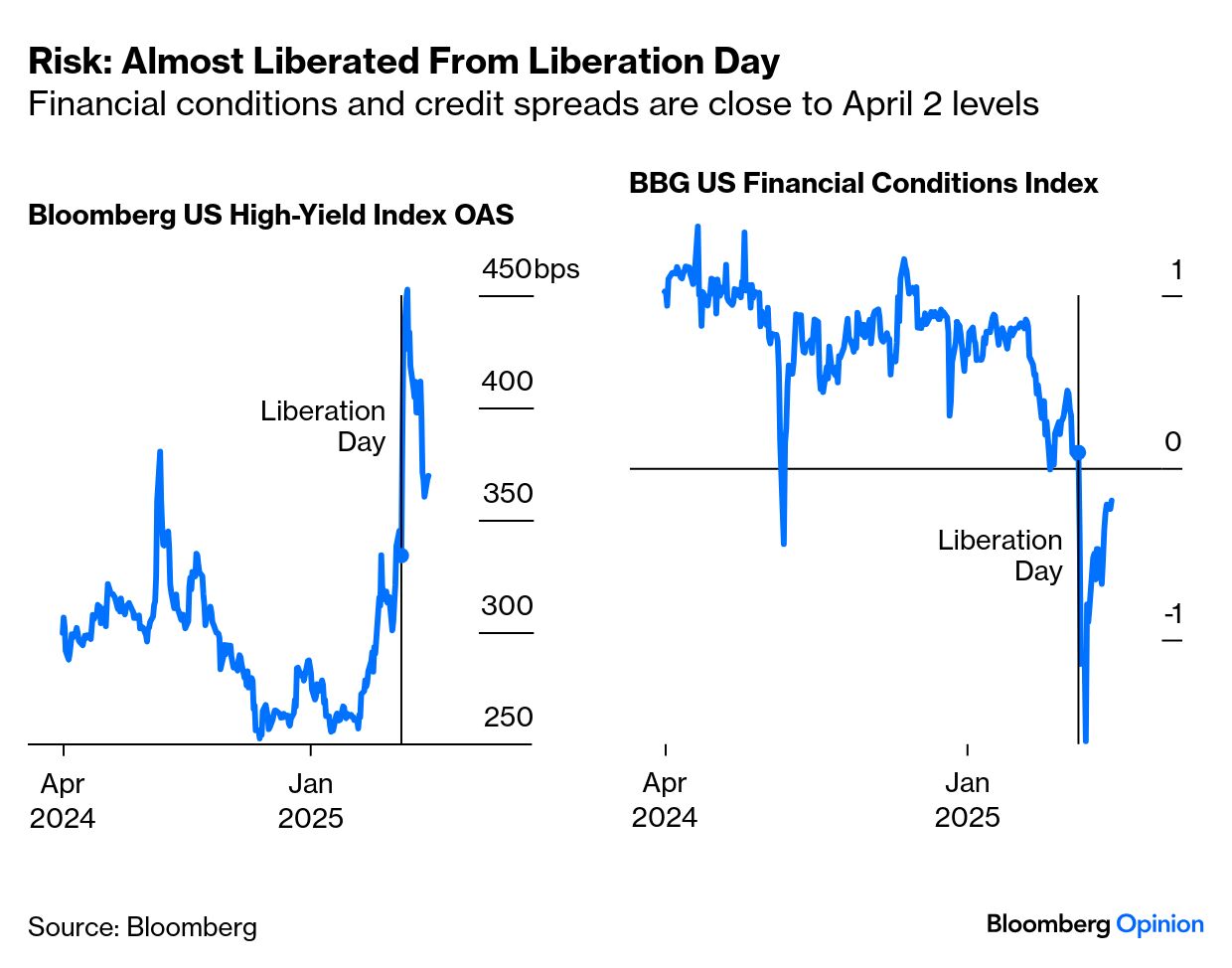

There are good reasons why stocks have recovered since April 2. But the current pricing seems to imply that the whole ghastly Liberation Day announcement can be made to go away as though it never happened. That is too hopeful, and the risks from now until July 8 are distinctly to the downside. |