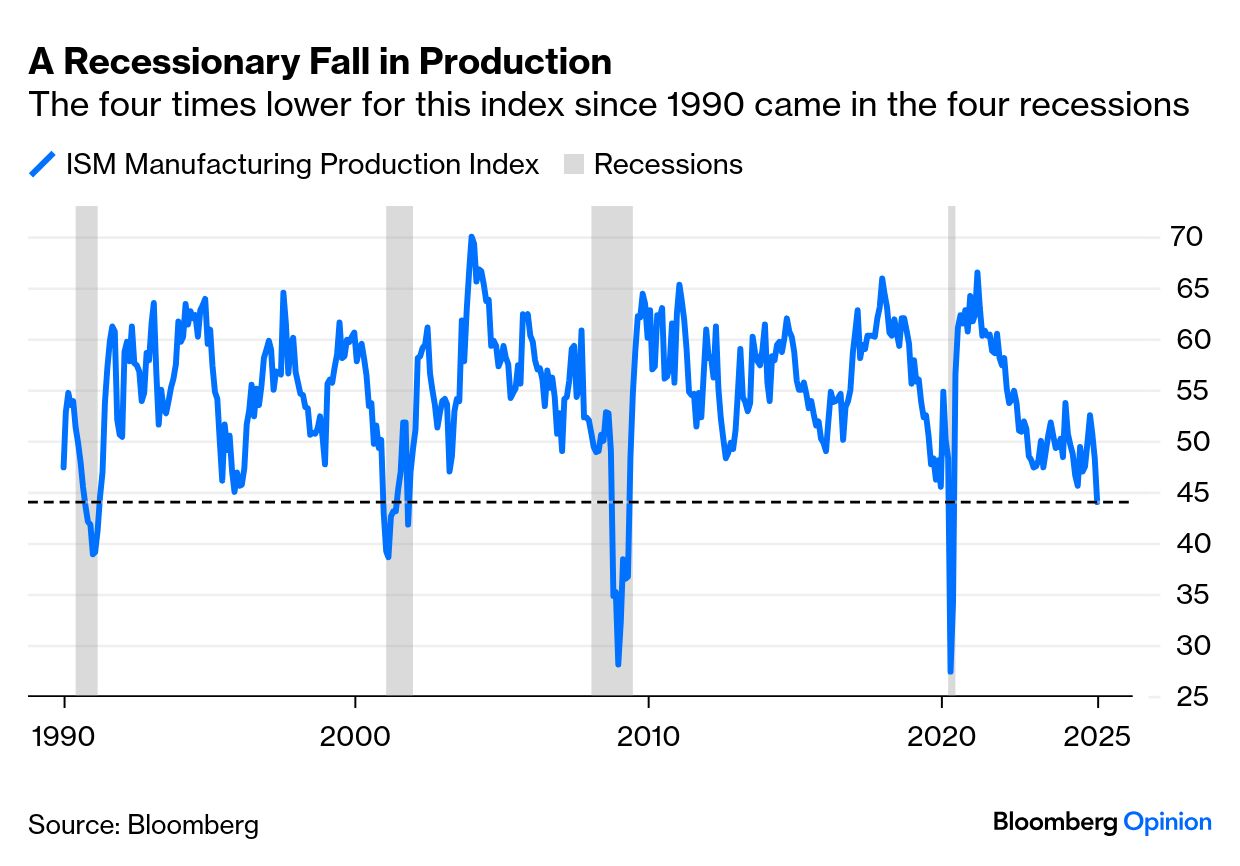

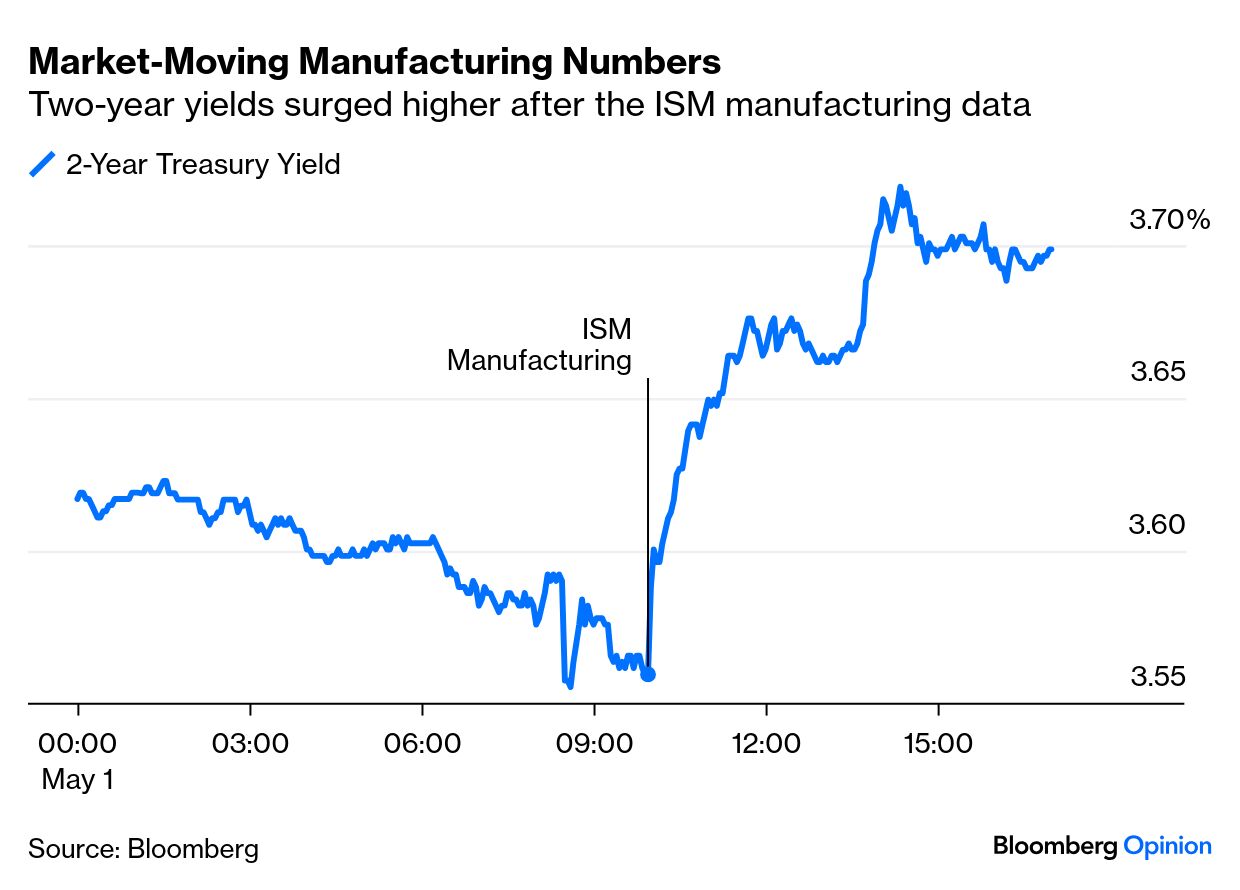

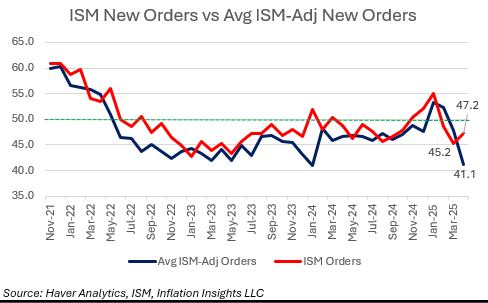

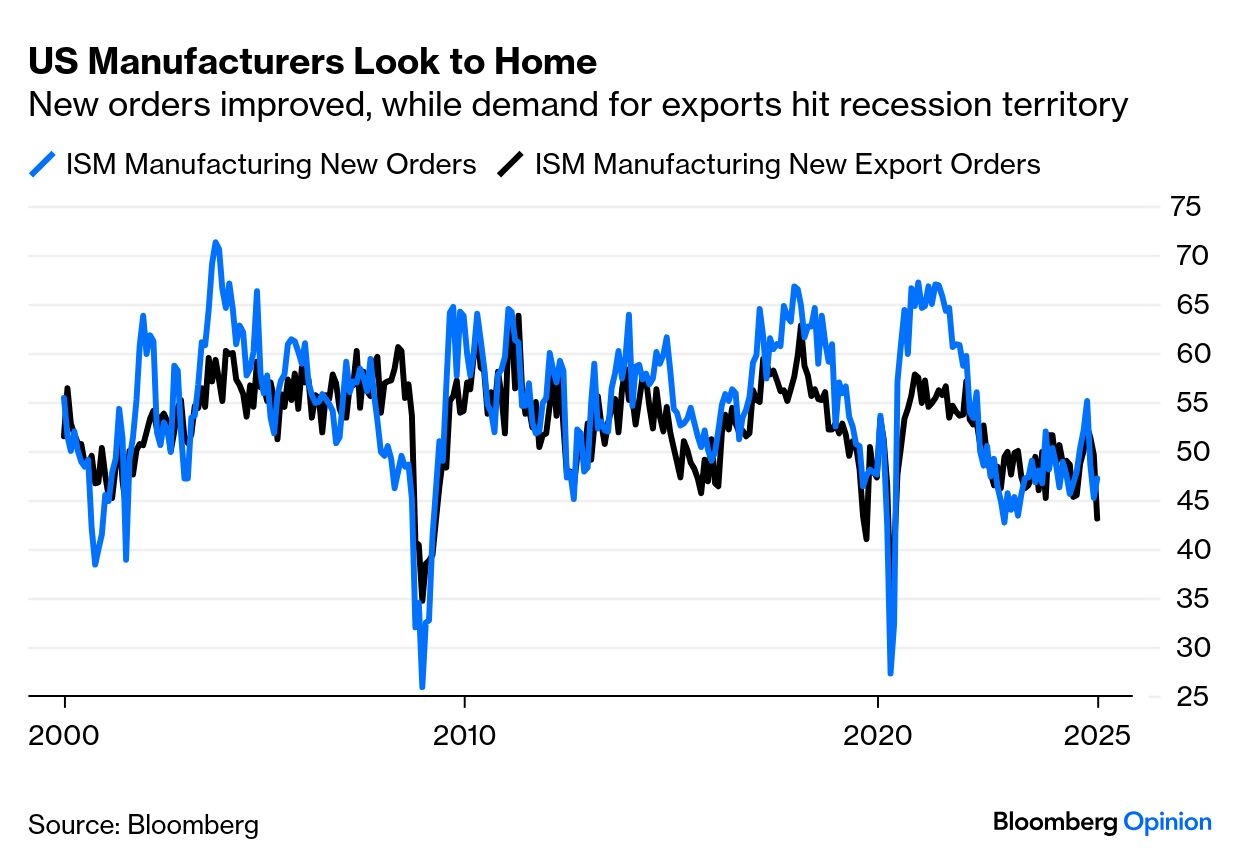

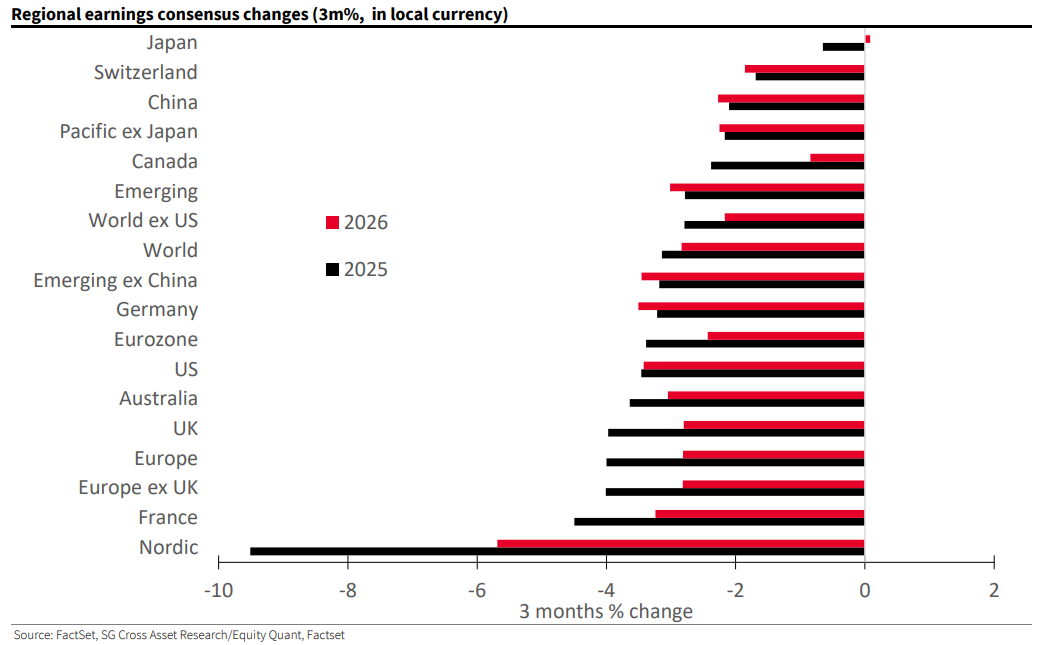

| When is an unambiguous recession indicator something investors can completely ignore? Answer: When tariffs are clouding perception so badly that nobody is quite sure of anything. That at any rate seems the conclusion as we approach the end of the first-quarter earnings season, while the hard economic data for April begin to roll in. The Institute of Supply Managers’ manufacturing index, long regarded as one of the best leading indicators of economic growth, was on the face of it alarming. The overall headline number is below the 50 that separates expansion from recession. Within it, the report on how much manufacturers were producing was downright alarming: These numbers don’t prove a recession is imminent, but they should certainly prompt risk managers and allocators to shift toward assets that do best in a downturn. That should mean bond yields go down. This is what happened to the two-year Treasury yield on Thursday: So, unmistakably negative manufacturing numbers caused a sharp rise in bond yields. Why? Mainly because of some bizarre inconsistencies in the report. The overall number wasn’t as bad as the consensus had predicted, largely because new orders were way ahead of estimates. What’s strange is that those estimates had been compiled by comparing with data from new orders coming out of the industrial surveys run by different branches of the Federal Reserve. In the following chart, from Omair Sharif of Inflation Insights LLC, the red line is the official ISM new orders number, while the dark blue shows the implied figure generated by the regional Fed surveys Sharif suggests the discrepancy may come from the survey’s different weightings, as the overall ISM is driven by sectors’ overall contribution to gross domestic product — so sectors such as chemicals or computers will take a greater weight. Another problem interpreting the data comes, inevitably, from tariffs. The overall new orders index improved slightly, but dropped for exports to a low previously seen only in recessions. Tariffs are meant to stimulate a shift of demand from exporters to domestic manufacturers, and they are perhaps already having that effect. It does make it harder to gauge the overall direction of the economy: Similar strictures apply to the earnings season. The first quarter’s results have generally been better than expected, by a greater margin than usual. But the direction of analysts’ estimates for the full year is unusually negative, as illustrated by Andrew Lapthorne, chief quantitative strategist at Societe Generale SA. The downgrade for the US is worse than for most, and Japan is the only spot of relative optimism: Downgrades like this are unusual. As Lapthorne summarized: Earnings are being downgraded, margins are under pressure and analysts are posting 2.5x more downgrades than upgrades in the S&P 500, a rarity during a reporting season. And this is all before we start incorporating tariffs impact.

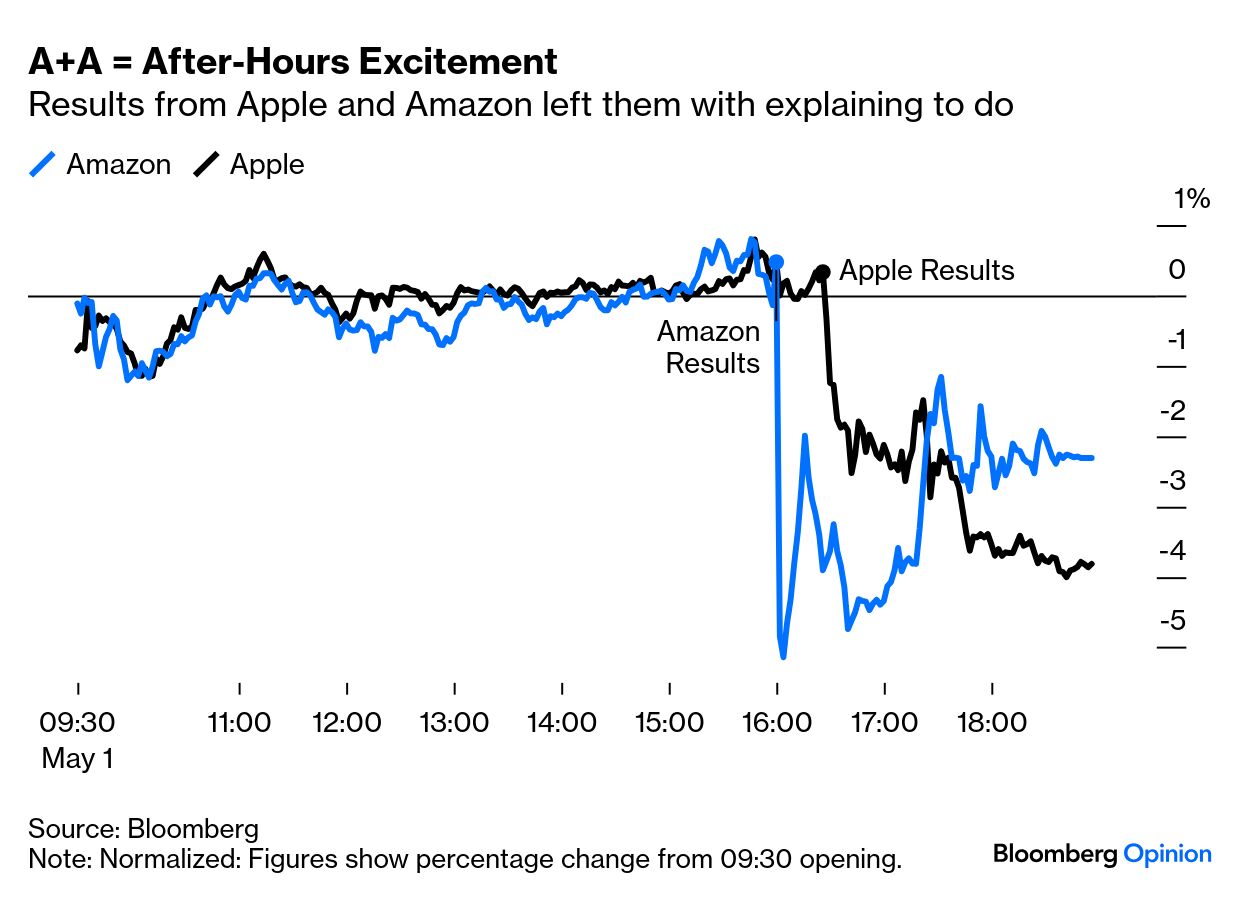

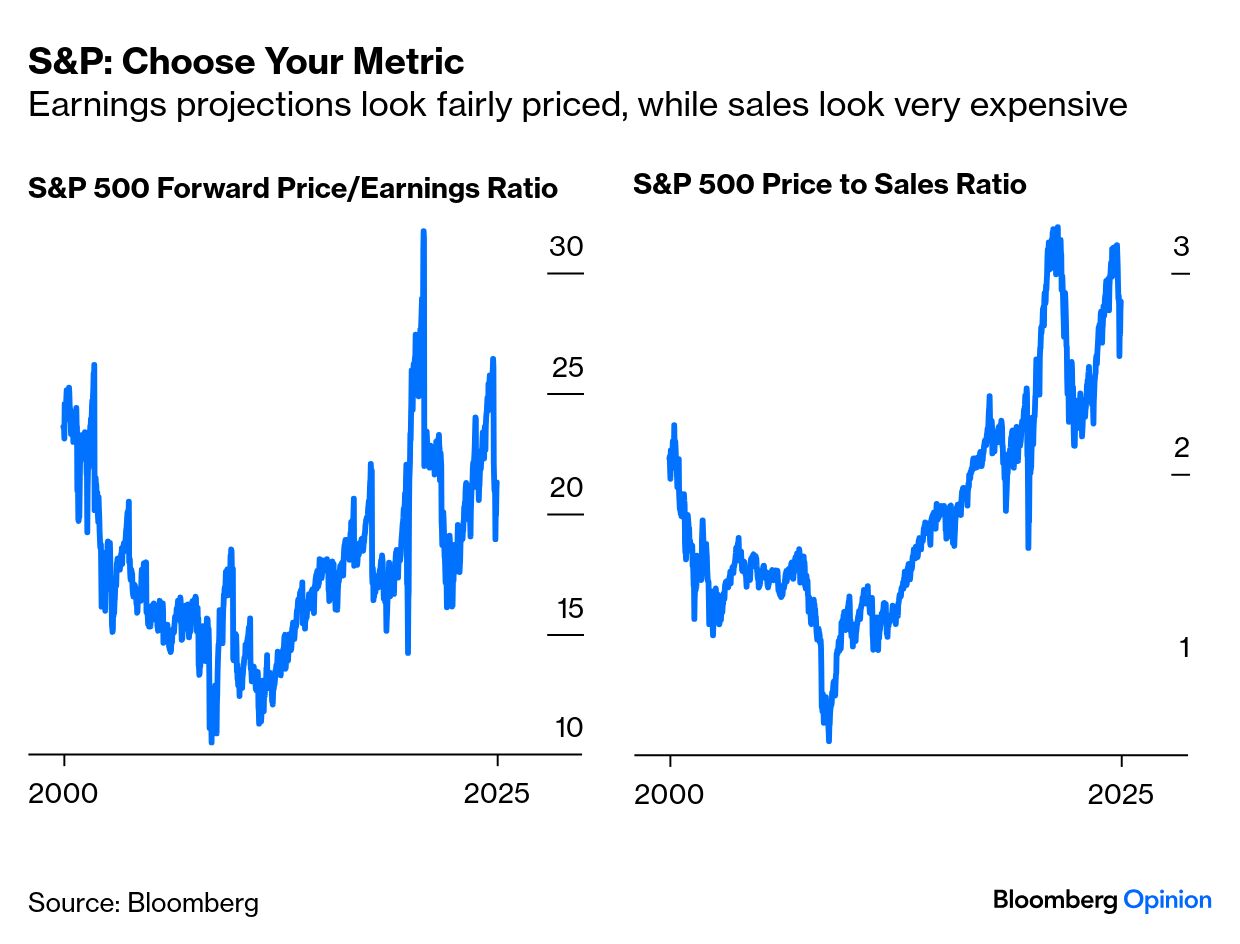

Thursday’s biggest corporate news came after the close as Amazon.com Inc. and Apple Inc. reported. Compared to the two Magnificent Seven companies that reported Wednesday, Meta Platforms Inc. and Microsoft Corp., their business models are far more directly exposed to international trade. Apple’s manufacturing is centered outside the US, and Amazon is a major importer. Wednesday’s M&M combination received a rapturous reception after hours. This is what happened to A&A: The problem for Apple was that it admitted that costs were rising — it estimates an extra $900 million thanks to tariffs in the next quarter — and that sales in China had disappointed. Amazon projected profits for the current quarter that were below prior expectations, thanks to the problems caused by tariffs. The stock recovered somewhat during the earnings call as executives emphasized that they were continuing to invest heavily in artificial intelligence, and had not yet noted any drop in demand due to tariffs. None of this suggests that this is a time to be too confident about anything — even though the market has now completed its recovery from the April 2 Liberation Day selloff. And it’s hard to say that the valuations reflect this. Compared to forward earnings, the S&P doesn’t seem particularly expensive, although it’s not cheap, either. Compared to sales, it looks massively overpriced: The two indicators have diverged because companies have managed to make steadily bigger profit margins. The market by implication is confident that those margins can continue. That suggests great confidence either that tariffs won’t happen, or that companies can cheerfully pass them on to their customers. Neither is a safe bet. Tariffs are creating confusion, as they had to. It’s probably best to treat the market recovery as a handy opportunity to make further transfers out of US stocks and into geographies that should be less affected. |