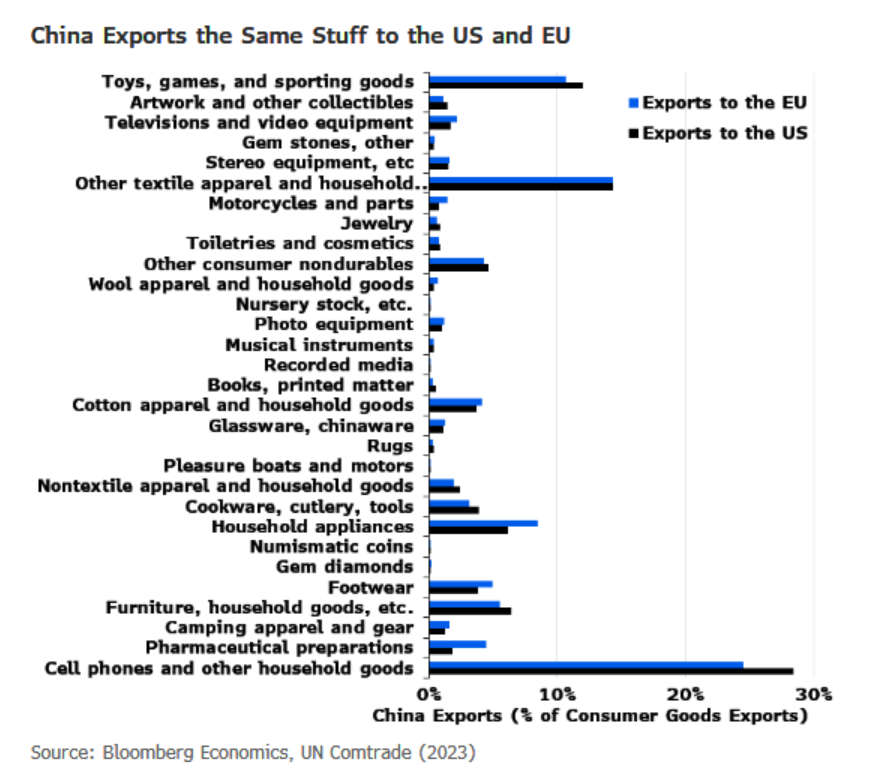

| I’m Craig Stirling, a senior editor in Frankfurt. Today we’re looking at the inflation impact on Europe of Chinese exports. Send us feedback and tips to ecodaily@bloomberg.net. And if you aren’t yet signed up to receive this newsletter, you can do so here. Chinese exports to the US, worth more than half a trillion dollars last year, are suddenly hitting a wall of tariffs imposed by the White House. So what happens when that tide rebounds on the world’s other major economic area, the European Union? That’s the question posed in a report this week by Bloomberg Economics. Jamie Rush, its chief European economist, has tried calculating the fallout on inflation in the region from Trump’s sudden jolting of global trade. The model he has created suggests that 85% of Chinese goods exports to the US will halt, and that only a third of that will then flow into alternative markets. But proportionately, that’s still $75 billion more imports into the EU. Given the consumer-focused nature of such goods, and the similarity in Chinese-sourced products bought in the region and the US, Rush’s reckoning is that it will have a material impact on inflation. His model suggests a cut in the level of prices by something between 0.5% and 1.5%. On an annual basis, the flood of imports could shave 0.4 percentage point off inflation. Consumer-price growth in the euro region is already close to the European Central Bank’s 2% target. Data out today showed an outcome of 2.2% in April. While the numbers were stronger than anticipated, the goal is still within sight. Euro-zone policymakers bracing for some sort of hit to economic growth from Trump’s tariffs on the bloc are already leaning toward further interest-rate cuts in due course to cushion the blow. Even without the impact of Chinese goods, officials could take some comfort in a more benign inflation backdrop, with the drop in the dollar driving a stronger euro that is curbing import costs, and crude oil noticeably lower. But add to that the prospect of even more downward pressure amid the global reverberations of Trump’s tariffs, and some Frankfurt policymakers could even start worrying about a repeat of the persistently price pressures that afflicted the euro region before the pandemic. “Diversion of Chinese exports from the US to other markets will inject some disinflationary pressure into the medium-term outlook,” said Rush. “That’s something the ECB will need to consider carefully.” Read the full research on the Bloomberg Terminal here. The Best of Bloomberg Economics | - Economists see a darkening outlook but are sticking by projections for two Federal Reserve rate cuts this year.

- Australian retail sales rose for a third straight month, driven by food-related spending, despite disruptions from a cyclone in northeastern Australia.

- South Korea’s consumer prices rose 2.1% in April, the same pace as last year, giving the central bank scope to consider resuming the rate-cut cycle.

- More than 180 companies have filed more than 1,100 individual requests for exclusions from Trump’s tariffs.

- Britain’s ballooning welfare benefits bill hasn’t been caused by the surge in hospital waiting lists since the pandemic, a study showed.

Amid all the discussion about the US dollar potentially losing some of its status in the global financial system, don’t conflate reserve-currency standing with the actual value of the dollar, says Steven Barrow, a longtime observer of the foreign-exchange market. “Since the advent of floating currencies in the early 1970s the dollar has gone through long cycles of depreciation as well as appreciation,” Barrow wrote in a note this week. “If the dollar has been improving its global dollar status over the past fifty-years or so” up to now, then “it has not shown up in the value of the dollar.” That said, Barrow does see depreciation coming, amid the potential for a US recession, a “deficit increasing budget” and speculation Trump may add to a reputation for Republicans being “more willing to get involved in bringing the dollar down when it is too high.” In short, he said, “the dollar could be on the verge of a multi-year downtrend – even if there’s no diminution of its dominant international status.” |