|

|

|

|

Good morning. The big banks posted stellar quarterly results last week, but not all is well in the industry. For too long, our regulators have prized stability over growth – unnecessarily so. This must change. That’s in focus today, along with the looming (potential) Air Transat strike. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tech: Microsoft vows to protect “digital sovereignty” in a $7.5-billion Canadian data-centre expansion during uncertain geopolitical times |

|

|

|

|

Mining: Anglo American scraps a controversial executive bonus plan tied to its proposed acquisition of Teck Resources on the eve of the shareholder vote for the deal |

|

|

|

|

Trade: U.S. and Canada discussed tariff-rate quota for steel before trade talks halted |

|

|

|

|

Investigating: Ontario Provincial Police launches probe into company that received more than $40-million from the provincial government |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Canada’s outsized fear of bank failures makes it harder for newer banks to enter the market, dampen innovation and raises costs for customers. Illustration by doomu

|

|

|

|

|

|

|

|

|

|

|

Fear is compromising our banking system |

|

|

|

|

I’m John Turley-Ewart, a contributing columnist for The Globe. I write about banking because few other industries have such an impact on the economy and the personal aspirations of Canadians. |

|

|

|

|

When a person walks through a bank’s doors, or logs in to their online banking account, they want to sustain their financial well-being. The experience matters. |

|

|

|

|

|

|

|

|

Much of this I learned working on the front lines in bank branches while at university and later in graduate school. Cashing cheques, paying bills, preparing money orders and opening accounts are, on the face of it, mundane tasks. |

|

|

|

|

But when you spend much of your day performing these services, meeting and talking with the people who need them, you see firsthand the special place a bank has in every person’s financial life. Providing mortgages, car loans and credit cards – even doing collection calls – only reinforced this. |

|

|

|

|

Money is personal, and when a bank fails to meet expectations, it can be taken personally. Expand that to the country and the banking system itself, and it is easy to understand that banking is also political. |

|

|

|

|

I was so struck by the personal and political aspects of banking that I decided to do a PhD in Canadian business history and focus primarily on banking, to trace how our banking system came to be and evolved over time. It has been at the centre of my intellectual curiosity ever since. |

|

|

|

|

I’ve learned that through this country’s banking history one can place a unique lens on the Canadian experiment itself. Canadians have looked to their banks as places of opportunity since the earliest days. National hopes and personal dreams have been made and denied in the many banks that have come, gone and persisted over time. |

|

|

|

|

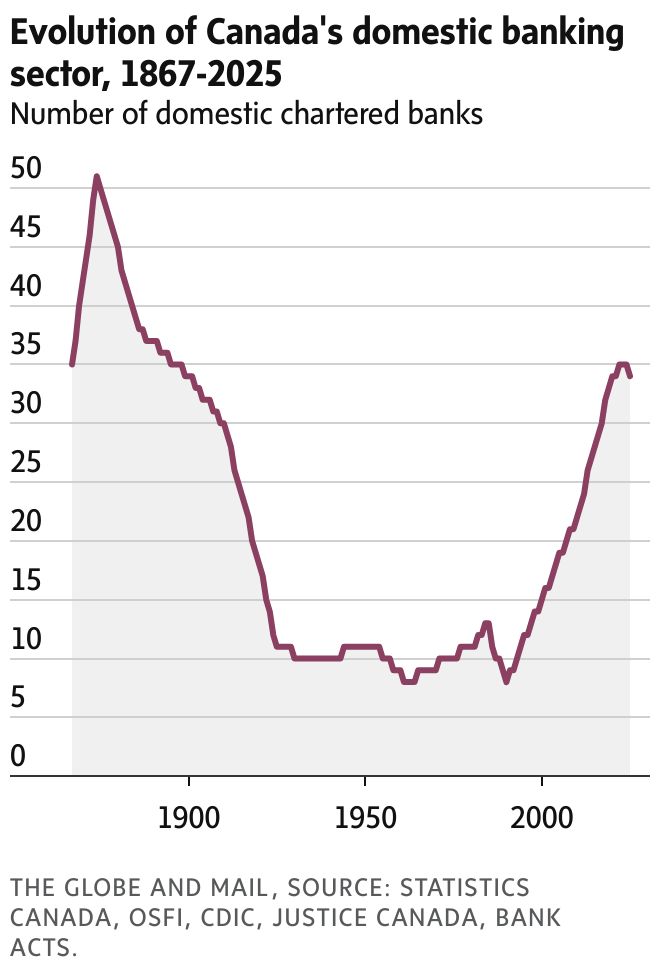

Bank failures have shaped the banking system we see today, in which six large banks control about 90 per cent of bank assets, while other, smaller banks struggle to grow and find their place. The concentration we see today is a conscious choice by Canadian governments. |

|

|

|

|

|

|

Compare that to the U.S, where over the past decade the country has seen roughly 70 new banks launched. Our number of banks continues to shrink. |

|

|

|

|

We have traded competition for stability, and the fear of bank failures persists today, driving new regulatory mechanisms and policies that make it harder for Canadian banks, large and small, to serve the economy and Canadian aspirations. |

|

|

|

|

This trend is a curious one given that we have not had a bank failure in 40 years. |

|

|

|

|

We look at one such instance of that trend today.

The domestic stability buffer is a special rainy-day reserve fund stacked atop other rainy-day funds that the largest banks are compelled to hold to cover potential losses, taking billions out of the economy in the process. This isn’t good for Canada, which would be better served by a system that saw rainy-day funds tailored to the actual risk banks are exposed to rather than a one-size-fits-all buffer. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The Globe and Mail

|

|

|

|

|

The Globe and Mail recently visited Save the Children in South Sudan to report on how one of the largest hunger crises in the world is poised

to become even worse. The crisis is the result of a number of factors including government corruption, escalating factional violence, extreme poverty and climate change, but it is further fuelled by a reduction in foreign aid from the United States and other Western countries. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|